- Markets in July

- Global market indices

- Currencies

- Cryptocurrencies

- Fixed Income

- Commodity sector news

- Key events in August

Markets in July

July was a tough month for US equity markets as small caps came to the fore in what appears to be the start of a rotation period as the Fed looks set to pivot towards rate cuts in September. Investors began to pull away from Technology and growth stocks during the month, uncertain about the ability of the Magnificent Seven to meet earnings expectations given their suggested spending on R&D in AI technology that may take longer than had been expected. However, there was some recovery on the last day of trading for the month as AI stocks such as Nvidia surged on and Meta also rose significantly on ad sales and signs that revenues were covering AI development costs.

The S&P 500 is +1.13% MTD, Dow is up +4.15% MTD, while Nasdaq is down -4.50% MTD. The NYSE is +3.79% MTD.

European equity markets were uniformly up in July. Like their US counterparts, they were affected by disappointing drops in Technology sector stocks. However, given their higher degree of internationalisation, they’ve also been hit by falling demand in China and other non-EU markets.

In the bond market, yields have decreased across both the US and Europe. Although the Fed decided, as was widely expected, to hold rates again yesterday at 5.25-5.50%, it has suggested that the risks are more balanced and the FOMC was “attentive to the risks to both sides of its dual mandate.” During the press conference following the announcement, Fed Chair Jerome Powell said, “A reduction in our policy rate could be on the table as soon as the next meeting in September.” The yield on the 2-year US Treasury note, which is closely tied to the Fed Funds rate, has fallen from 4.74% in June to 4.36% at the end of July. The benchmark 10-year US Treasury note yield has declined to 4.035% from June's 4.56%. In Europe, the 10-year German bunds yield has dropped 19.6 basis points (bps), and the UK 10-year yield has also fallen, dropping by 20.7 bps.

The Economic Picture

The US economy is still powering ahead, coming in at 2.8% GDP growth in Q2, double the rate of Q1. Consumer spending, which accounts for more than two-thirds of the economy, increased at a 2.3% rate after slowing to a 1.5% rate in Q1. Labour costs are up +4.1% on an annual basis while wages and salaries increased 4.2% on an annual basis, slowing from the first quarter’s 4.4%. Nevertheless, the labour market is cooling. The July JOLTs and ADP reports both indicate that private hiring is slowing: job openings dropped 46,000 to 8.184 million in June. Private payrolls rose by only 122,000 jobs in July after advancing by an upwardly revised 155,000 in June. The unemployment rate rose to 4.1% in June from 4.0% in May. Labour costs are likely to cool further as the jobs market continues to ease. The inflation rate was 3% for the 12 months ending June, compared to the previous rate increase of 3.3%. The personal consumption expenditures (PCE) price index, excluding the volatile food and energy components, was 2.9% in Q2, significantly lower than the 3.7% pace in Q1.

Despite the expected slowdown in the labour market, consumer sentiment indicators suggested an improvement in consumer confidence in July. The Conference Board's consumer confidence index rose in July to 100.3 from a downwardly revised 97.8 in June. The Expectations Index, based on consumers’ short-term outlook for income, business, and labor market conditions, was at 78.2 in July, up from 72.8 in June. However, the Present Situation Index, which is based on consumers’ assessment of current business and labour market conditions, declined to 133.6 from 135.3 last month. In addition, the University of Michigan's consumer sentiment index declined for the third consecutive month, reaching 65.6 in June 2024, its lowest level since November, down from 69.1 in May. The current conditions gauge fell to 62.5 from 69.6, and the expectations sub index decreased to 67.6 from 68.8. While year-ahead inflation expectations remained steady at 3.3%, the five-year outlook edged up to 3.1% from 3%.

The flash Composite PMI Output Index in July was at 55.0, up from June’s 54.8 and a 27-month high. The Flash US Services Business Activity Index for July came in at 56.0, also up from June’s 55.3, a 28-month high. The service sector outperformed manufacturing for a fourth straight month. The Flash US Manufacturing PMI showed that business activity in the manufacturing sector is contracting, as it came in at 49.5, a noticeable drop from June’s 51.6 and a 7-month low. The rate of increase of average prices charged for goods and services continued to slow, dropping to a level consistent with the Fed’s 2% target.

Uncertainty still surrounds the timing of the ECB second interest rate reduction although markets are largely expecting a rate cut in September. Growth across the eurzone is improving, coming in at 0.3% in the three months to the end of June. However, Germany, the region’s largest economy, contracted 0.1% because of a drop in investment in equipment and buildings.

The eurozone unemployment rate remains at 6.40%, but wage pressures persist as a concern. This is notable in light of the euro area's annual inflation rate, which rose to 2.6% in July 2024 from 2.5% in June. Core inflation, which excludes more volatile energy, food, alcohol and tobacco prices, was at 2.9% in July, unchanged from June. On the growth front, the eurozone HCOB flash Composite PMIs for July fell to 50.1 in from 50.9 in June, pointing to a near-stagnation of private sector activity. Output in Germany decreased for the first time in four months, while companies in France reported a third consecutive monthly reduction in business activity while the rest of the euro area grew at the slowest pace since January.

In the UK, inflationary pressures continued to subside in June, with the headline rate at 2.0% year-on-year. While core inflation measured 3.5%, services prices remained elevated at 5.7%. Concurrently, unemployment edged up to 4.4% from 4.3%, while the annual growth in total earnings (including bonuses) was 5.7%.

On the growth front the UK continued to surprise. The S&P Global Flash UK PMI Composite Output Index rose to 52.7 in July from 52.3 in June, signalling a solid upturn in private sector activity. The flash Services PMI also rose. It came in at 52.4, up from June’s 52.1 and a 2-month highs. Consumer sentiment is showing signs of improvement, as evidenced by the GfK Consumer Confidence Survey, which indicated a rise in the confidence index to -13 in July, a one point increase from June. Notably, two measures were up, one was down and two were unchanged in comparison to June’s numbers. Retail sales volumes experienced a significant 43% year-on-year drop in July 2024, an even steeper decline than the 24% decrease recorded in June, according to the latest Confederation of British Industry (CBI) Distributive Trades Survey.

The BoE decided to cut rates by 25 basis points today in a very close 5-4 vote.Overall price pressures are easing but service sector prices remain high despite the falling headline inflation and a weakening labour market. There are also increasing expectations of inflation rising back to 2.7% later this year according to the latest BoE forecasts.

Global Market Indices

US:

S&P 500 +1.13% QTD and +15.78% YTD

Nasdaq 100 -4.50% QTD and +11.71% YTD

Dow Jones Industrial Average +4.15% QTD and +8.10% YTD

NYSE Composite +3.79% QTD and +11.02% YTD

The Equally Weighted version of the S&P 500 posted a +4.39% this month, its performance is +8.64% YTD, 7.14 percentage points lower than the benchmark.

The S&P 500 Utilities sector is the top performer this month at +6.73% MTD +14.82% YTD, while the Communication Services sector is -4.16% MTD, and +20.85% YTD.

Stocks and government bonds experienced a significant rally on the final trading day of July, concluding a volatile month for global markets with substantial gains. All three major indexes opened higher and maintained their momentum following the Fed’s decision to maintain interest rates and Chair Jerome Powell's indication of potential rate cuts in September if inflation continues to decline.

The technology-focused Nasdaq Composite index surged 2.6%, marking its most robust performance since February. The S&P 500 index advanced 1.6%, while the Dow Jones Industrial Average saw a more modest increase of 0.2%. Notably, the S&P 500 achieved its strongest performance on a Fed day in two years.

The Russell 2000 index, July's top performer, registered a 0.5% gain, slightly trailing other indexes after outpacing them in recent weeks. Despite this, the Russell 2000 concluded the month with a remarkable 10% increase, its best showing of the year.

Wednesday's trading activity demonstrated that investor confidence in major technology companies remains steadfast. Nvidia, the prominent player in the AI sector, saw its shares soar 13%. Micron Technology also experienced a gain of 7.1%. Other semiconductor companies rallied as well, recovering from some of the sharp declines that characterised trading in July.

Q2 earnings season in focus.

The S&P 500’s blended net profit margin for Q2 2024 is 12.6%, surpassing the year-ago figure (11.6%), the 5-year average (11.5%), and the previous quarter's result (11.8%). It is only the second instance since Q2 2022 that the index has exceeded a 12% net profit margin.

On a sector level, six sectors experienced year-over-year increases in net profit margins for Q2 2024 compared to Q2 2023. Financials led this growth (18.4% vs. 16.7%), followed by Information Technology (24.9% vs. 23.3%) and Communication Services (13.4% vs. 11.9%). Conversely, five sectors saw y/o/y decreases, with the Real Estate sector experiencing the most significant decline (35.0% vs. 36.7%).

The S&P 500 is expected to maintain net profit margins above 12.0% for the remainder of 2024, with estimated figures of 12.4% for both Q3 and Q4.

According to LSEG I/B/E/S data, y/o/y earnings growth for the S&P 500 in Q2 is projected to be 12.6%. This number jumps to 13.6% when excluding the Energy sector. Of the 283 companies in the S&P 500 that have reported earnings to date for Q2 2024, 78.4% have reported earnings above analyst estimates, with 56.5% of companies reporting revenues exceeding analyst expectations. This falls short of the historical average of 62.2% and the last four quarters’ average of 62.3%. The y/o/y revenue growth is projected to be 5.0% in Q2, decreasing to 4.8% when excluding the Energy sector.

Health Care, at 93.3%, was the sector with most companies reporting above estimates, and with a surprise factor of 8.1%, it’s the sector that’s beaten earnings expectations by the highest surprise factor. Within the Communication Services sector, only 58.3% of companies have reported above estimates. The Consumer Discretionary sectors’ earnings surprise factor is the lowest at 0.1%. The S&P 500 surprise factor is 4.2%. The forward four-quarter price-to-earnings ratio (P/E) for the S&P 500 sits at 21.0x.

Europe:

Stoxx 600 +1.13% QTD and +8.18% YTD

DAX +1.50% QTD and +10.49% YTD

CAC 40 +0.70% QTD and -0.15% YTD

FTSE 100 +2.50% QTD and +8.21% YTD

IBEX 35 +1.11% QTD and +9.53% YTD

FTSE MIB +1.84% QTD and +11.24% YTD

In Europe, the Equally Weighted version of the Stoxx 600 is +2.95% in July, and its performance is +5.80% YTD, 2.38 percentage points below the benchmark.

The Stoxx 600 Construction & Materials is the leading sector this month, up +6.20% MTD +6.27% YTD, while Technology has exhibited the weakest performance at -6.05% MTD and +9.87% YTD.

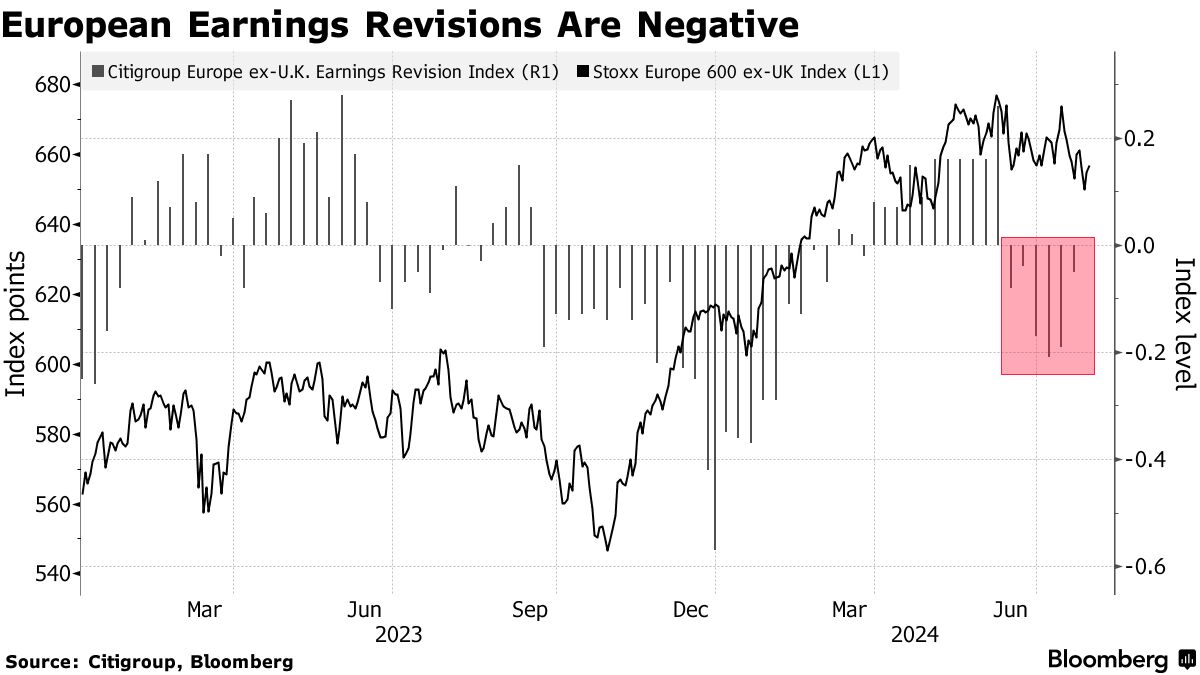

Europe's cautious optimism: earnings season delivers growth but raises concerns.

Bank of America's analysis reveals that Europe's Q2 earnings season is poised to deliver the first positive EPS growth in six quarters. However, the outlook is tempered by companies adjusting profit targets downward due to weakened demand. Recent concerns have centred around the European luxury goods sector and automakers, due to subdued demand from China.

Approximately 40% of the largest European firms have reported so far, with earnings growth tracking at 4%, slightly surpassing the 3% consensus expectation. However, guidance cuts are at their highest levels since at least Q2 2023, a development that Bloomberg suggests could undermine expectations of a 4% y/o/y rise in the STOXX 600 for 2024.

Forward-looking Purchasing Managers' Indexes (PMIs) have been weak, reflecting a contraction in manufacturing and slower expansion in the services sector. There is some suggestion that while guidance in growth sectors has met or exceeded forecasts, the uneven trends in cyclical sectors will have a more significant impact on future performance.

STOXX 600 Earnings Q2 2024.

As of 30th July, according to LSEG I/B/E/S data for the STOXX 600, Q2 2024 earnings are expected to increase 1.9% from Q2 2023. Excluding the Energy sector, earnings are expected to increase 1.0%. Q2 2024 revenue is expected to increase 0.2% from Q1 2023. Excluding the Energy sector, revenues are expected to increase 0.9%. Of the 152 companies in the STOXX 600 that have reported earnings by 30th July for Q2 2024, 53.9% reported results exceeding analyst estimates. In a typical quarter 54% beat analyst EPS estimates. Of the 179 companies in the STOXX 600 that have reported revenue by 30th July for Q2 2024, 58.7% reported revenue exceeding analyst estimates. In a typical quarter 58% beat analyst revenue estimates.

Health Care, at 73%, is the sector with most companies reporting above estimates. Financials, at 13%, is the sector that beat earnings expectations by the highest surprise factor. In the Real Estate sector only 25% of companies reported above estimates. Technology’s earnings surprise factor was the lowest at -7%. The STOXX 600 surprise factor is 5.2%. The forward four-quarter price-to-earnings ratio (P/E) for the STOXX 600 sits at 13.3x.

During this week, 40 companies are scheduled to report quarterly earnings.

Global:

MSCI World Index +1.70% QTD and +12.70% YTD

Hang Seng -2.30% QTD and +1.54% YTD

Mega cap stocks had a mixed performance in July with Microsoft -6.40%, Meta Platforms -5.83%, Alphabet -5.82%, Nvidia -5.28%, and Amazon -3.24%, while Apple +5.44%, and Tesla +17.28%.

Energy stocks experienced a positive performance this month, with the Energy sector +2.03% in July and +11.31% YTD. WTI was -9.77% and Brent -4.25% in July. Baker Hughes Company +10.09%, Apa Corp +5.94%, Phillips 66 +3.05%, ExxonMobil +3.01%, Halliburton +2.66%, Chevron +2.59%, Marathon Petroleum +2.04%, Shell +0.21%, while Energy Fuels -4.58%, and Occidental Petroleum Corporation -3.51%.

Phillips 66 Q2 earnings. On Tuesday, 30th July, Phillips 66 reported Q2 adjusted EPS of $2.31 surpassing FactSet's estimate of $1.98. The company also exceeded expectations for Adjusted EBITDA ($2.18 bn vs. FactSet $1.93 bn) and midstream NGL fractionated volumes (744 MBD vs. 679 MBD q/q). See Report.

Initial reactions were positive, citing strong midstream and chemical EBITDA, better-than-expected refinery throughputs, record NGL pipeline and fractionation volumes, substantial returns to shareholders ($1.325 bn), and a smaller-than-expected renewables loss.

Phillips 66 reaffirmed its commitment to returning over 50% of CFO to shareholders, targeting $13 bn - $15 bn in shareholder returns by the end of 2024. The company emphasised its ongoing focus on cost reductions, primarily through structural changes driven by employee-led initiatives, resulting in $600 million in cost savings.

Phillips 66 reaffirmed its 2025 EBITDA target of $14 bn based on mid-cycle conditions and ongoing projects. The recent Pinnacle acquisition further strengthens the company's midstream strategy, providing immediate earnings from fee-based contracts.

Baker Hughes Q2 earnings. On 26th July, Baker Hughes reported Q2 adjusted EPS of $0.57, exceeding FactSet's estimate of $0.49. The company also surpassed expectations for revenue ($7.14 bn vs. FactSet $6.81 bn) and adjusted EBITDA ($1.13 bn vs. FactSet $1.05 bn), while orders reached $7.53 bn, surpassing the year-ago figure of $7.47 bn. See Report.

The company raised its full-year EBITDA guidance by 5% at the midpoint, implying $2.4 bn versus the street's estimate of $2.3 bn. Baker Hughes highlighted that the results marked the highest quarterly non-LNG equipment bookings in its history.

Analysts responded positively to the update, emphasising the beat across all segments, increased 2024 guidance, returns to shareholders ($375 mn through dividends and buybacks), and strong orders, particularly in the Industrial & Energy Technology (IET) segment, which led to a record backlog.

Baker Hughes outlined its long-term guidance, aiming for high-teens EBITDA margins in the second half of 2024, reaching 20% in both the Oilfield Services and Equipment (OFSE) segment by 2025 and the IET segment by 2026. The company anticipates continued growth in international oilfield services into 2025, driven by the gas infrastructure and Floating Production Storage and Offloading (FPSO) markets, and expects new energy orders to be fueled by technologies across CO2 and hydrogen projects.

During the earnings call, Baker Hughes projected a 150 basis points increase in margin expansion for 2024 and reiterated its expectation of a 20% revenue increase in the IET segment due to stronger revenue and margin improvements. The company also highlighted significant contributions from carbon capture, utilisation, and storage (CCUS) projects to new energy orders. While the LNG market remains strong, Baker Hughes affirmed its $12B order expectation for the year, driven by robust non-LNG orders.

BP Q2 earnings. On 30th July, 2024, BP reported a Q2 underlying replacement cost net profit of $2.76 bn, exceeding the consensus estimate of $2.54 bn. The company declared a dividend of approximately 8.0 cents per ordinary share and announced a $1.75 billion share buyback program. See report.

Q2 underlying replacement cost profit before interest and tax reached $5.41 bn, slightly below the consensus forecast of $5.54 bn. Production stood at 2,379 thousand barrels of oil equivalent per day (Mboe/d), surpassing FactSet's estimate of 2,347.9 Mboe/d.

The company declared an interim dividend of approximately 8.0 cents per ordinary share, exceeding the consensus of 7.6 cents, with payment expected on 20th September, 2024. In connection with the Q2 results, BP intends to execute a $1.75 bn share buyback before reporting Q3 results and remains committed to announcing a $3.5 bn buyback for H2 of 2024.

As part of its commitment to return at least 80% of surplus cash flow to shareholders, BP plans share buybacks of at least $14 bn through 2025.

BP outlined its long-term guidance, targeting $800 million to $1 billion in renewable natural gas (RNG) revenue by 2030, constructing 5 to 10 hydrogen plants this decade, reaching peak liquids production in the Permian Basin around 2027, establishing a partnership in Lightsource BP within 12 to 18 months post-acquisition, and stabilising production around 2 million barrels per day towards 2030. The company emphasised its focus on cash flow and returns rather than production volume.

During the earnings call, BP noted that it is on track to achieve its $2 billion cost reduction target, with $0.5 billion in savings expected by 2025. The company aims to align unit production costs with its portfolio mix, targeting around $6 per barrel by mid-2025. The transitional engine EBITDA is expected to be bolstered by the Bunge acquisition, aiming for nearly $2 billion starting in 2025. The convenience and electrification sectors are projected to deliver around $1.5 billion, with EV charging nearing breakeven. BP anticipates margin improvement in the biofuel sector through the end of 2025 and into 2026, driven by rising mandates and potential import duties in Europe. The Archaea biogas business is experiencing strong market pricing and demand growth, with new plants increasing production capacity.

Occidental announces progress on divestiture and debt reduction program. On Monday, 29th July, Occidental Petroleum Corporation announced significant progress in its divestiture and debt reduction program. The company revealed an agreement to sell certain Delaware Basin assets in Texas and New Mexico to Permian Resources for approximately $818 million. In addition, Occidental disclosed the completion of several other dispositions totaling approximately $152 million in 2024. All proceeds from these sales will be allocated towards reducing the company's debt.

This announcement follows Occidental's previously stated plan to execute a $4.5 billion to $6 billion divestiture program within 18 months of closing the acquisition of CrownRock, anticipated to occur in August.

The assets to be sold to Permian Resources encompass approximately 27,500 net acres in the Barilla Draw Field of the Texas Delaware Basin and approximately 2,000 net acres in the New Mexico Delaware Basin. Combined net production for Q4 of 2024 is estimated at approximately 15,000 barrels of oil equivalent per day.

The transaction with Permian Resources is expected to close in Q3 2024, contingent upon standard closing conditions.

Chevron-Hess merger delayed until mid-2025 due to arbitration.Chevron’s $53 billion acquisition of Hess is expected to face further delays, with the transaction not anticipated to close until mid-2025 due to a pending arbitration hearing scheduled for May 2025. The mega-deal encountered complications when ExxonMobil asserted its right of first refusal over Hess's stake in a profitable oil project situated off the coast of Guyana, resulting in an arbitration process between the two energy giants.

In a statement, Chevron noted, "Chevron and Hess had both anticipated and requested an earlier hearing date, but the arbitrators' schedules did not permit this." Following this announcement, shares in both companies experienced a slight decline in extended trading.

Energy earnings this week. Shell (Earnings of $6.01 bn, EPS Factset estimate $0.94) is scheduled to report Q2 earnings today, while Chevron (Adjusted Earnings of $5.45 bn, EPS Factset estimate $2.93) is expected to report on 2nd August before the markets’ open.

Materials and Mining stocks had a positive month in July. The Materials sector was +4.31% in July and +7.58% YTD. Gold prices remained relatively high in July, +4.24% MTD +17.65% YTD, but copper continued downwards, -5.25% MTD. Newmont Mining +17.20%, Sibanye Stillwater +5.78%, Celanese Corporation +4.64%, Nucor Corporation +3.07%, Mosaic +3.01%, and Yara International +1.11%, while Freeport-McMoRan -6.56%, and Albemarle -1.94%.

Shifting trends in China's gold market. China's gold consumption in the first half of 2024 decreased by 5.61% compared to the same period in 2023, according to data released by the Gold Association on Sunday. It attributed the decline primarily to high prices, stating that "high gold prices have increased the operational risk for gold processing and sales enterprises." This led to a decrease in wholesale and retail purchases, as well as a significant reduction in the processing volumes of jewellery. Gold jewellery consumption, which accounts for 51.6% of total consumption, fell by 26.68% y/o/y to 270.02 tons in the first half.

Elevated prices also impacted the central bank's bullion purchases, with China abstaining from gold acquisitions for a second consecutive month in June.

However, the demand for gold bars and coins surged by 46.02% to 213.64 tons during the same period, representing 40.8% of total consumption. This increase can be attributed to renewed investor interest in safe-haven assets amid ongoing geopolitical conflicts and a sluggish global economic recovery.

China's gold output from domestically produced raw materials increased by 0.58% y/o/y to 179.63 tons in the first half. However, the Gold Association noted that "the output increase missed expectations because the easily mined resources in old mines gradually reduced while the construction of new mines faced problems." Additionally, "some miners scaled down or shut down production amid increasingly stringent environmental and safety requirements."

Gold output from imported raw materials rose by 10.14% to 72.03 tons, bringing China's total gold output in the first half of the year to 251.66 tons, a 3.14% increase compared to the same period in 2023.

Albemarle Q2 earnings. On 31st July, Albemarle Corporation reported Q2 adjusted EPS of $0.04, significantly below FactSet's estimate of $0.43. Revenue for the quarter reached $1.43 bn, surpassing FactSet's projection of $1.34 bn, while adjusted EBITDA amounted to $386.4 million, exceeding the FactSet estimate of $281.2 million.

Albemarle maintains its prior full-year outlook considerations, which are based on observed lithium market price scenarios. The company expects the previously published $15/kg range to hold even if lower July market pricing persists for the remainder of the year. This is attributed to enterprise-wide cost improvements, robust volume growth, increased shipments from the Talison joint venture, and strong performance in Energy Storage contracts.

However, Albemarle has revised its capital expenditure expectations, now anticipating spending to be at the high end of the $1.7 bn to $1.8 bn range due to timing adjustments.

Following a comprehensive review of its cost and operating structure, Albemarle announced strategic asset and cost actions designed to enhance its long-term competitiveness. These actions include placing Kemerton Train 2 in care and maintenance, halting construction on Kemerton Train 3, and prioritising the optimization and ramp-up of Kemerton Train 1. As a consequence of these measures, Albemarle expects to record a charge ranging from $0.9 billion to $1.1 bn as an exceptional item in its Q3 2024 results.

Newmont Corporation Q2 earnings. On 24th July, Newmont Corporation reported Q2 adjusted EPS of $0.72, surpassing FactSet's estimate of $0.62. The company's revenue reached $4.40 bn, exceeding FactSet's projection of $4.13 bn, while adjusted EBITDA amounted to $1.97 bn, also surpassing the FactSet estimate of $1.88 bn. Newmont produced 1.6 million attributable gold ounces and 477,000 gold equivalent ounces (GEOs) from copper, silver, lead, and zinc, including 38,000 tonnes of copper.

Newmont aims to generate at least $2 bn from non-core asset sales, excluding Lundin and Batu Hijau. Reclamation spending is expected to return to historical levels by 2028-2029, and the share repurchase program may be extended beyond the initial $1 bn commitment.

During the earnings call, Newmont highlighted that the asset sales process is progressing as planned, with competitive bids received for Telfer and North American assets. Phase 2 of the asset sale is nearing completion, and strong buyer interest has been noted. The company has transparently addressed tailings issues at Telfer, which are not expected to impact the sale value. Share buybacks will be determined by free cash flow and divestiture proceeds, and the board may consider extending the program beyond the $1 bn cap. Newmont expects to realise $130 million in synergies, primarily from supply chain efficiencies, by Q4 2025. The company's annual guidance reflects the impact of the Lihir autoclave shutdown, and major reclamation at Yanacocha is factored into long-term financials.

Commodities

Oil prices had a disappointing July with WTI -9.77% MTD and Brent -4.25% MTD. This was largely due to increasing concerns about Chinese demand, more US rigs in operation, and limited impact from geopolitical tensions in the Middle East.

The US administration looks to replenish strategic reserves amid lower oil prices.

The Biden administration is seeking additional funding to purchase more oil to replenish the depleted US Strategic Petroleum Reserve (SPR). The administration has been gradually replenishing the SPR, which reached a four-decade low following an unprecedented drawdown due to Russia's invasion of Ukraine. Ove the past two years the administration repurchased 43.25 million barrels of oil, including a recent announcement of 4.65 million barrels. However, with approximately $1.2 billion remaining in the designated purchasing account, Deputy Energy Secretary David Turk stated that the administration would like to acquire more than the estimated 15 million barrels this amount would cover.

The Energy Department is engaging with Congress to secure additional funds for further crude oil purchases. It is also requesting that Congress cancel additional mandated reserve sales, a strategy previously employed to halt 140 million barrels in sales scheduled through fiscal year 2027. Turk noted that 100 million barrels in sales remain on the books that the department wants removed. Deficit hawks in Congress may demand offsets to compensate for lost revenue, potentially complicating the process.

The administration's efforts coincide with a decline in crude prices, which have fallen approximately 10% since early April, reaching levels below the White House's stated buying range of $79 a barrel and below. The Energy Department has been refilling the reserve at an average purchase price of $77 a barrel and has accelerated the return of 5.5 million barrels loaned to oil companies.

ExxonMobil and Macquarie were awarded the contracts announced on Monday, with oil deliveries to the SPR's Bayou Choctaw storage site scheduled from 1st October through 31st December. The SPR currently holds 375 million barrels of oil, compared to approximately 600 million barrels at the start of 2022.

US oil production declines as gasoline demand reaches post-pandemic records.

In May, US oil demand reached a seasonal record as American drivers consumed the highest volume of gasoline since the pre-pandemic era, according to data released on Wednesday by the US Energy Information Administration (EIA).

Total crude oil and petroleum product supplied, a metric used by the EIA to gauge demand, experienced a month-over-month increase of 792,000 barrels per day (bpd) in May. This represents the highest monthly figure since last August and was a record high for the month of May.

Gasoline demand alone surged to a post-pandemic peak of 9.40 million bpd, the highest level since August 2019. Gasoline demand in the US traditionally peaks during the summer driving season.

Conversely, crude oil production experienced a reduction of 61,000 bpd, reaching 13.18 million bpd in May. This decrease was attributed to lower output from the Federal Offshore Gulf of Mexico and North Dakota, which counterbalanced record production levels in Texas and New Mexico.

Currencies

The dollar depreciated this month amid escalating expectations of the commencement of monetary easing by the Fed at its September meeting. A sequence of economic prints have eased the path for the anticipated Fed’s soft landing scenario, while growing optimism for a UK and European recovery have strengthened the British pound and Euro.

The GBP is +1.65% YTD against the USD. The BoE cut rates 25 basis points today in a 5-4 vote. However, despite inflation reaching the 2% target for two months running, core inflation is at 3.5%, services inflation remains high, coming in at 5.7% in June, well above expectations, and growth has been better than expected. The unemployment rate has risen by 0.6 % to 4.4%. Headline inflation is expected to rise again this year to 2.7%. The BOE now expects growth of 1.25% this year, more than double the pace it expected in May.

The EUR is +1.16% YTD against the USD. The ECB made its first 25 bp cut in June and is widely expected to cut again in September. However, wage pressures remain as the eurozone labour market remains tight, with unemployment at record low levels, unchanged at 6.4% in June.

Cryptocurrencies

Bitcoin +7.77% MTD, +8.22% 3 Months and +54.54% YTD

Ethereum -4.41% MTD, +9.21% 3 Months and +41.56% YTD

Nine Spot Ethereum ETFs began trading on 23rd July. However, despite an initial inflow of over $100 million on the first day of trading, they have continued to be hit by outflows from the incumbent Grayscale Ethereum Trust. The outflow of funds from the new Ethereum ETFs according to SoSoValue data, is now at -$483.18 million as of 31 July, with total net assets at $9.08 billion, approximately 2.34% of the Ethereum market cap. Although Ethereum has underperformed this month, Bitcoin had a positive July. It was boosted by macroeconomic data indicating that the US Federal Reserve is increasingly likely to begin its rate cutting cycle in September, thereby making cryptocurrencies more attractive. We have also seen increasing focus on cryptocurrency in the wider economy by US Presidential candidates. Republican nominee and former President Donald Trump promised thousands of Bitcoin enthusiasts at the Bitcoin 2024 conference in Nashville, Tennessee tthat as president he would make America “the Bitcoin superpower of the world.” He has also promised to fire SEC chair Gary Gensler, who has been an ardent critic of cryptocurrency products, and create a strategic Bitcoin reserve.

Note: As of 6:30pm EDT 31 July 2024

Fixed Income

US 10-year yield -36.7 basis points QTD +15.4 basis points YTD to 4.035.

German 10-year yield -19.6 basis points QTD +29.6 basis points YTD to 2.305%.

UK 10-year yield -20.7 basis points QTD +43.1 basis points YTD to 3.970%.

US Treasury 10-year bond yields were -36.7 basis points (bps) in July, reaching 4.035%.

Market expectations for a September rate cut by the Fed have increased this month following the Fed’s statement, with CME's FedWatch Tool fully pricing a reduction of at least 25 bps, an increase from the 59.02% recorded at the end of June. Swap traders are pricing in a total of almost 70 bps worth of reductions for the year.

The benchmark German 10-year yield was -19.6 bps in July at 2.305%, while the UK 10-year yield was -20.7 bps through July at 3.970%. The spread between US 10-year Treasuries and German Bunds contracted by -17.1 bps from 30th June, it currently stands at 173.0 bps.

Italian bond yields, a benchmark for the eurozone periphery, were -42.4 bps this month to 3.647%. Consequently, the spread between Italian and German 10-year yields contracted -22.8 bps to 134.2 bps from 157.0 bps last month.

The futures market places a more than 90% chance of a quarter-point rate cut from the ECB at its next policy meeting in September, having kicked off its easing cycle in June.

Note: Data as of 5pm EDT 31 July 2024

What to think about in August 2024

Carry trade risks escalate amid yen volatility and BoJ's shift towards tightening.

The Japanese yen strengthened further following hawkish remarks by BoJ Governor Ueda. USD/JPY rate reached an overnight low of ¥149.63, a level not seen since 19th March. This continued yen strength was attributed to Ueda's openness to further rate hikes during his press conference on Wednesday, 31July. Significantly, there was no revision of rate hike forecasts, which were largely concentrated around October before Wednesday's surprise move. The BoJ reaffirmed inflation forecasts above its target which may also leave the door open for further action.

Recent developments in yen carry trades have been discussed amidst anecdotal evidence of unwinding positions. While some investors are sceptical that a small rate hike would have a significant impact, carry trades are known to be sensitive to rate directionality and volatility. Overnight implied volatility for USD/JPY surged to 27% on Wednesday, reaching its highest level year-to-date. Following the BoJ rate hike, the US-Japan rate differential is expected to narrow further, reinforced by expectations of a September Fed cut after the FOMC meeting. CFTC data shows short yen positions are 40% below their April peak but remain elevated at $8.61 billion.

Post-close data released on Wednesday showed FX intervention totaling ¥5.535 trillion ($36.9 billion) from 27th June to 29th July, broadly in line with expectations. Widespread suspicions of intervention arose after the yen spiked in mid-July, with estimates based on money market data suggesting a total of ¥5.71 trillion. This latest MOF action differed from earlier rounds as the dollar was already declining due to surprisingly soft US CPI data. The momentum was further fueled by Japanese officials urging BoJ rate hikes to curb yen weakness.

A 30th July Bloomberg interview with newly appointed FX chief Atsushi Mimura indicated little change in strategy compared to his predecessor, Masato Kanda. Mimura reaffirmed that action would be taken if necessary after considering multiple factors, referencing the G20 agreement on FX reaffirmed at the Brazil summit. He also hinted at continuing Kanda's strategy of keeping investors guessing about intervention operations.

July FOMC maintains rates, acknowledges moderating job gains and inflation risks.

As widely expected, the July Federal Open Market Committee (FOMC) meeting ended with no adjustment to the benchmark interest rate, which remains at 5.25 - 5.50%. While there was no explicit indication of a September rate cut, the policy statement contained notable dovish modifications.

The statement acknowledged that inflation remains "somewhat elevated." Additionally, it noted that "job gains have moderated," a change from the previous characterisation of "job gains have remained strong." The committee also stated that it remains "attentive" to inflation risks, a shift from the prior language of "highly attentive."

Furthermore, the statement highlighted the dual risks to both sides of the Fed's mandate on inflation and employment, underscoring the complex economic landscape. Finally, the statement reiterated the Fed's stance of awaiting greater confidence before implementing rate cuts, aligning with Fed Chair Powell's recent hesitance to commit to a specific timeline and data-dependent approach.

The subsequent press conference offered no major surprises. Powell acknowledged that a rate cut could be possible in September, but also noted a scenario where no rate cuts occur in 2024. Initial economist analyses suggest that the August Jackson Hole symposium could provide another opportunity for the Fed to signal a policy shift.

Key events in August

The potential policy and geopolitical risks for investors that could negatively affect corporate earnings, stock market performance, currency valuations, sovereign and corporate bond markets and cryptocurrencies include:

1 August 2024 Bank of England, Monetary Policy meeting. Interest rate futures show a roughly 60% chance of a quarter-point rate cut during today’s meeting. Markets are anticipating another rate cut this year. Headline inflation has been at the BoE's 2% target in May and June, growth has been stronger, coming in at 0.4% in May, and is expected to be 1.1% this year. However, there are still concerns about policymakers balancing signs of a weakening labour market with stubbornly high inflation in the services sector.

19-22 August 2024 US Democratic Party National Convention, USA. Delegates are due to meet in Chicago to essentially endorse Kamala Harris as the party’s nominee for President as she has the support of enough delegates to win the nomination. Her Vice-Presidential pick, expected to be announced sometime around the 6th of August, will also be endorsed at the convention. Harris is, according to the latest Economist poll, just trailing former President and Republican nominee Donald Trump.

22-24 August 2024 Jackson Hole Economic Symposium, Jackson Hole, Wyoming, USA. At this annual meeting organised by the Federal Reserve Bank of Kansas City, the focus will be on "Reassessing the Effectiveness and Transmission of Monetary Policy." Attendees will include Fed Chair Jerome Powell and other global central bank heads.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供给您仅供信息参考之用,不应被视为认购或销售此处提及任何投资或相关服务的优惠招揽或游说。